Feedback: UK and Nordic countries confirm their lead in Open-banking

FACTS

- Mastercard has just published a report on the progress of open banking in Europe, called "Open Banking Readiness Index: The Future of Open Banking in Europe".

- Unsurprisingly, the UK and the Northern countries stand out for their lead in this field.

- Methodology: Mastercard has conducted a study on 10 European countries (United Kingdom, France, Italy, Spain, Germany, Denmark, Norway, Sweden, Poland and Hungary) in order to analyze the state of the art in Open-banking at a local level and to compare the progress of each country in this field.

- Several criteria are reviewed in this report:

- the general characteristics of connectivity and access to digital services for residents,

- the progress of regulation,

- the readiness of the digital banking infrastructure,

- notable open-banking and API initiatives in the country,

- banking maturity.

- It finds that the UK and Nordic countries are best positioned to make the most of Open-banking thanks to a high number of banking APIs, but also progressive regulators and better consumer readiness.

- The report also highlights key differences in how countries approach open banking:

- France, Italy, Spain: open-banking is driving the digital transformation of domestic payment ecosystems ;

- Germany: a collaborative approach specific to the country to foster open banking development

- Denmark, Norway, Sweden: Nordic collaborative model build on the P27 initiative to provide a common open banking system across countries;

- Poland, Hungary: the open banking system is used as a vehicle to renew legacy banking infrastructures.

CHALLENGES

- The push for an open banking system towards a more global approach to finance is driven by several factors: consumer pressure, regulatory obligations, and a greater awareness of privacy concerns.

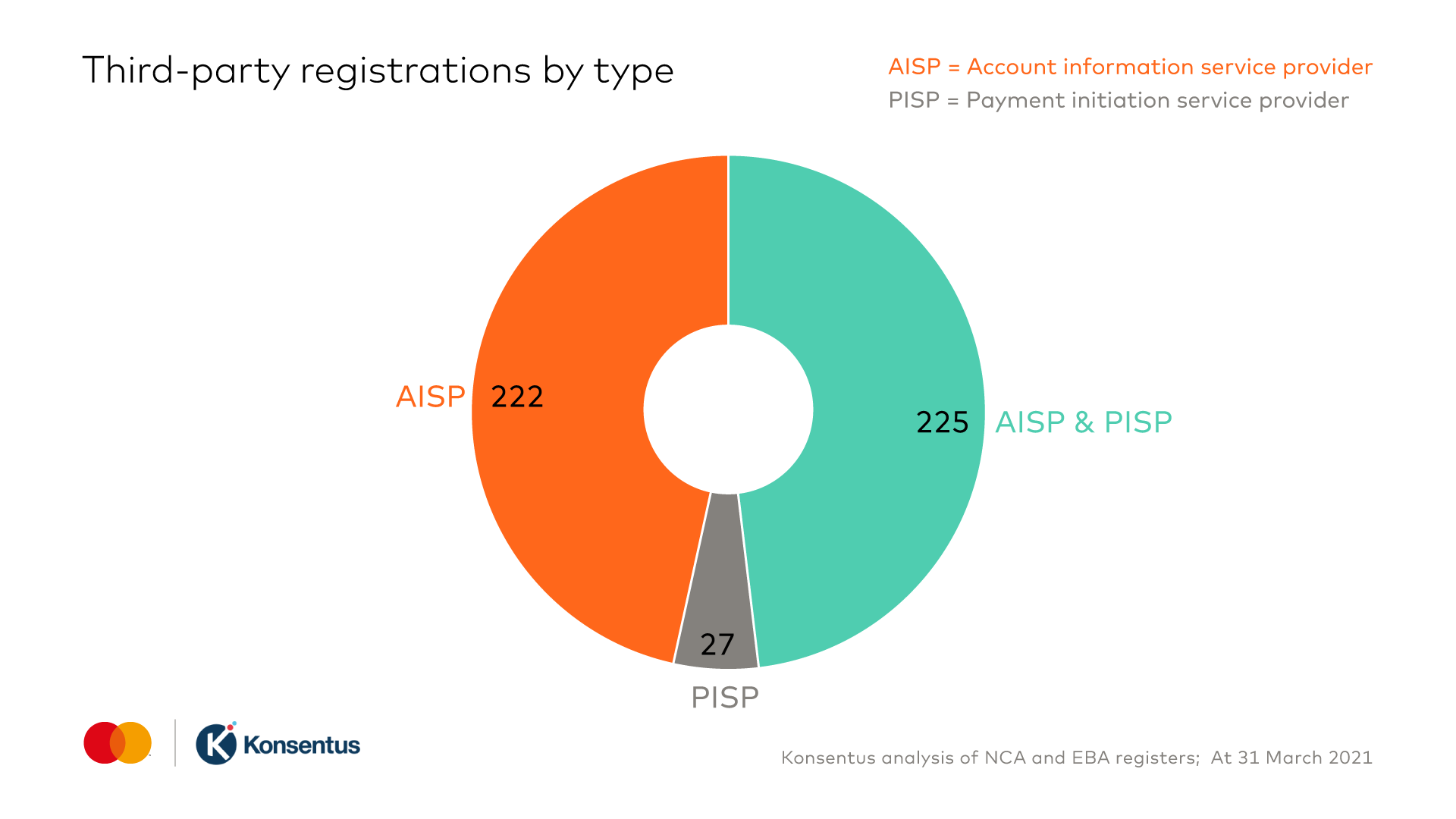

- An obvious finding: the Open Banking Implementation Entity (OBIE), established by the UK Competition and Markets Authority (CMA) in 2016 to provide open banking services, found that Uk counts around 294 FinTech and PSPs. 102 of them, have direct offering on the market. This dynamism was further confirmed by the fact that the UK just welcomed its 100th unicorn, positioning the country at the forefront of innovation in financial services and especially in Open-banking. In addition, payment API volume in the U.K. increased by more than 70 percent between Q4 2020 and Q1 2021, to exceed 2 billion API calls for the first time this year.

- A singular approach : Collaborative models between the Nordic countries, through the P27 initiative for example, contribute to their progress. P27 is a joint initiative of Danske Bank, Handelsbanken, Nordea, OP Financial Group, SEB and Swedbank, exploring the possibility of establishing a pan-Nordic payment infrastructure for domestic and cross-border payments in the Nordic currencies and the euro. The name P27 comes from the project's goal of improving payments for the 27 million people in the Nordic countries.

MARKET PERSPECTIVE

- OBIE published statistics on the use of open banking technologies last October. The country is clearly ahead of the game and the use cases have been developed in particular with the availability of data from the 9 main British banks (AIB, Bank of Ireland, Barclays, Danske, HSBC, Lloyds, Nationwide, RBS and Santander).

- British players are making their mark on the subject internationally, such as the British Banking-as-a-Service platform Railsbank, which has just signed a major transatlantic partnership with the American FinTech Plaid.

- The Nordic countries, meanwhile, can rely on references that have managed to establish themselves on a European scale. Tink has just confirmed its lead, as the FinTech announced the signing of a partnership with Novalnet to develop a payment initiation service in Europe.