Xiaomi Aims for the Indian Credit Market

The Chinese smartphone manufacturer Xiaomi introduces Mi Credit, their first ever launch of a credit offer in India, a promising market for credit services where customer demand keeps growing. This offer was designed in partnership with the lending platform KrazyBee and relies on a micro-credit model similar to the one applied to their “Mi Credit” service in China.

Xiaomi entered India in 2014 through proposing food products and technological items (smartphones, connected bracelets). This country came to become their second-largest market, after China, contributing up to 32% to their $18 billion overall turnover in 2017, via three out of their five sales channels.

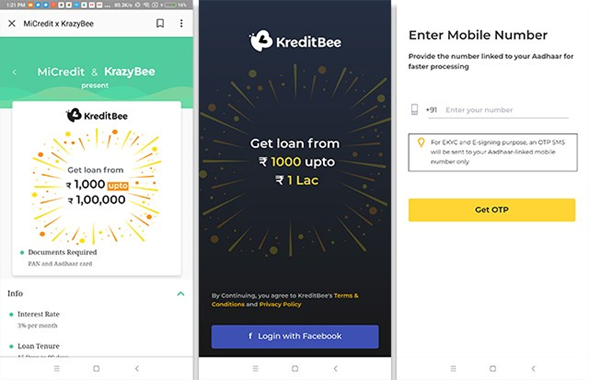

They now unveil a credit offer soon to be made available officially. This service will be proposed to Indian employees for amounts ranging from 1,000 to 100,000 rupees, over 15 to 90 days, and a monthly 3% interest rate will apply. These loans are only granted to MIUI users (Xiaomi-distributed Android OS). And they are granted instantly since the applicant’s biometric-based Aadhar number is included in the decisioning process.

The user specifies some personal information, then the scoring process is triggered and he is informed of the maximum amount he may be lent. Xiaomi also tries to further invest on this market: in October 2017, they led a funding round for KrazyBee and are planning to invest $1 billion in roughly 100 Indian start-ups, throughout the next five years.

Comments – India: a promised land for foreign investors

Through this launch, the Indian credit market is again put in the spotlight. Investors see this country as a highly promising market, especially as most of the population is still poorly addressed by traditional financial institutions and not everyone has access to credit offers. Some industry players understood this well and began focusing on this region: Tala and PayU, for instance).

Foreign investors already aimed for payments-related sectors, and some of them –such as Xiaomi– are trying to enter the market for financial services, too. These launches may also be viewed as ways for them to expand their ranges of products, while standing out as viable new entrants to challenge local institutions. These institutions, as it happens, have a hard time adjusting their offers.

As for the Chinese manufacturer, they are expanding their action scope beyond just mobile media, through value-added services (“Mi Video”, “Mi Music”, and “Mi Credit”), this strategy has already been implemented on their home market.